[ad_1]

The month-to-month survey of building purchasers signifies a slight improve in business exercise in March, ending a six-month interval of decline.

Survey respondents typically commented on a turnaround in gross sales pipelines and higher new enterprise enquiries linked to the bettering financial outlook and extra secure monetary situations. New orders additionally seem to have expanded on the quickest tempo since Might 2023. Nonetheless, building firms remained cautious about hiring workers, with employment numbers falling for a 3rd consecutive month.

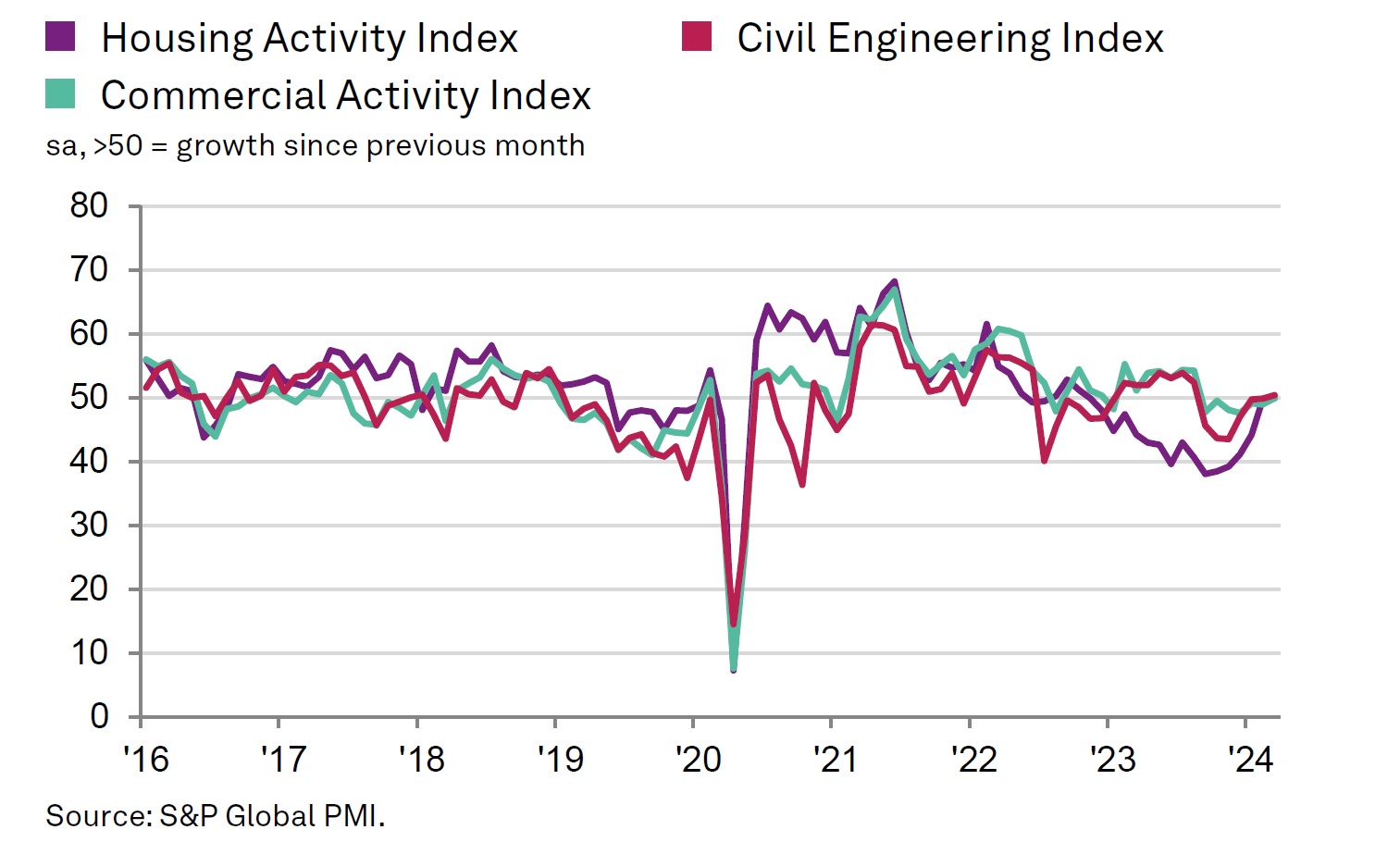

The headline S&P World UK Building Buying Managers’ Index (PMI) rose from 49.7 in February to 50.2 in March. Any studying above 50.0 signifies an total enlargement of building output. Though signalling solely a fractional rise in enterprise exercise, the index

was in optimistic territory – indicating progress – for the primary time since August 2023.

Civil engineering was the best-performing phase in March, as output ranges elevated at a marginal tempo. Panel members cited elevated work on infrastructure tasks and resilient demand within the power sector.

Home-building and industrial building exercise had been each broadly unchanged in March. The stabilisation in residential work represented the very best efficiency for this class since November 2022.

March information pointed to a modest improve in new work obtained by building firms. The speed of enlargement accelerated since February and was the strongest for 10 months. Anecdotal proof pointed to a common rise in new venture begins and higher tender alternatives throughout the development sector thus far in 2024.

In distinction to the optimistic traits for output and new orders, the March survey signalled one other discount in staffing numbers. That mentioned, the speed of job shedding was solely marginal and was much less unhealthy than in February . On the identical time, subcontractor utilization was secure in March. Charges charged by subcontractors elevated on the quickest tempo since August 2023.

Buying prices rose for the third month operating in March. Nonetheless, the speed of inflation was solely marginal and the weakest seen over this era. Survey respondents famous rising transport prices, however others recommended that robust competitors amongst suppliers had constrained the general price of enter worth inflation.

Suppliers’ supply occasions shortened for the 13th consecutive month in March, albeit solely reasonably. Anecdotal proof recommended that bettering supplies availability and subdued demand had contributed to bettering vendor efficiency.

Building firms stay upbeat about their prospects for enterprise exercise within the subsequent 12 months. Practically half (49%) of the survey panel anticipate an increase in output ranges, whereas solely 11% predict a decline. Nonetheless, expectations have deteriorated noticeably: in February, 51% mentioned they anticipated an increase and solely 6% predicted a decline. Political uncertainty, squeezed margins and monetary pressures had been cited as components weighing on optimism.

Tim Moore, economics director at S&P World Market Intelligence, which compiles the survey, mentioned: “UK building output returned to progress in March as a renewed enlargement of civil engineering work was supported by extra secure situations within the housing and industrial constructing segments. The marginal total rise in whole building exercise ended a six-month interval of contraction.

“The near-term outlook for building workloads seems more and more beneficial as order books improved once more in March and to the best extent for slightly below one yr. Building firms typically commented on a broad-based rebound in tender alternatives, helped by easing borrowing prices and indicators that UK financial situations have began to recuperate within the first quarter of 2024.

“Workers hiring was a weak spot for the development sector in March amid lingering issues about margin pressures and continued threat aversion amongst main shoppers. Building corporations typically reported delays with changing departing workers, which led to a lower in whole employment numbers for the third month in a row.

“Provide chain pressures eased throughout the development sector as subdued buying exercise helped to alleviate strains on capability. Improved provide situations additionally led to a slowdown within the price of value inflation, which slipped to a three-month low in March.”

Brian Smith, head of value administration at Aecom, mentioned: “The development business’s stoop has fortunately stopped in need of the seven-month mark, in time for extra beneficial climate situations and with among the monetary pressures it has confronted in current occasions easing.

“With inflation persevering with to fall, the Financial institution of England has opened the door to price cuts anticipated within the subsequent few months, easing finance prices which can increase the willingness of builders to push ahead with paused tasks.

“There stay challenges for building corporations within the quick time period. An more and more aggressive tendering market is predicted to stay for remainder of this yr and, though some enter prices are falling, labour shortages and the ensuing worth rises are challenges that can stay.”

Atul Kariya, head of actual property and building at accountancy group MHA, mentioned: “Whereas the slight rise in at this time’s building PMI information is optimistic information and displays improved sentiment from an admittedly low base, it’s definitely not an indication of sustained restoration within the sector, and situations stay difficult.

“Exercise within the industrial sector is choosing up steadily though sometimes contracts are frequently being deferred to later within the yr. Housebuilders have had a combined 2024, with the yr beginning properly however a subsequent dip in February and March. Regardless of the drop in home costs final month reported this morning by Halifax our shoppers are anticipating that sentiment will enhance as we head into late Spring and early Summer season, because it sometimes does yearly, as pressures are easing with rates of interest most likely peaking, mortgage charges falling once more, and materials and labour prices stabilising, providing a window of alternative to the sector.

“Nonetheless, to make sure a sustained restoration for the housing business the essential fundamentals have to vary. The shortage of political stability, comparatively excessive company tax compared with rivals like Eire, and the related value of capital within the UK are making it a much less beneficial possibility for actual property traders. The following authorities, of no matter political persuasion, must set out a five-year plan to help the business and make the UK enticing to traders as soon as once more.”

Obtained a narrative? Electronic mail information@theconstructionindex.co.uk

[ad_2]